Inside the shifting perceptions of those building Europe’s SAF future

Survey insights from Shell, Lufthansa, OMV, SkyNRG and others on what’s driving confidence, and what’s not.

During the recent Sustainable Aviation Futures Congress in Amsterdam, we ran a short perception survey on-site, asking industry professionals about the current state and future outlook of sustainable aviation fuel (SAF) in Europe.

Respondents from organisations including Shell, Lufthansa Group, SkyNRG, OMV, T&E, Oxford University, and the Royal Air Force offered revealing perspectives on the disconnect between current production pathways and sustainability expectations, the credibility of industry commitments, and the effectiveness of emerging policy tools.

Key takeaways at a glance:

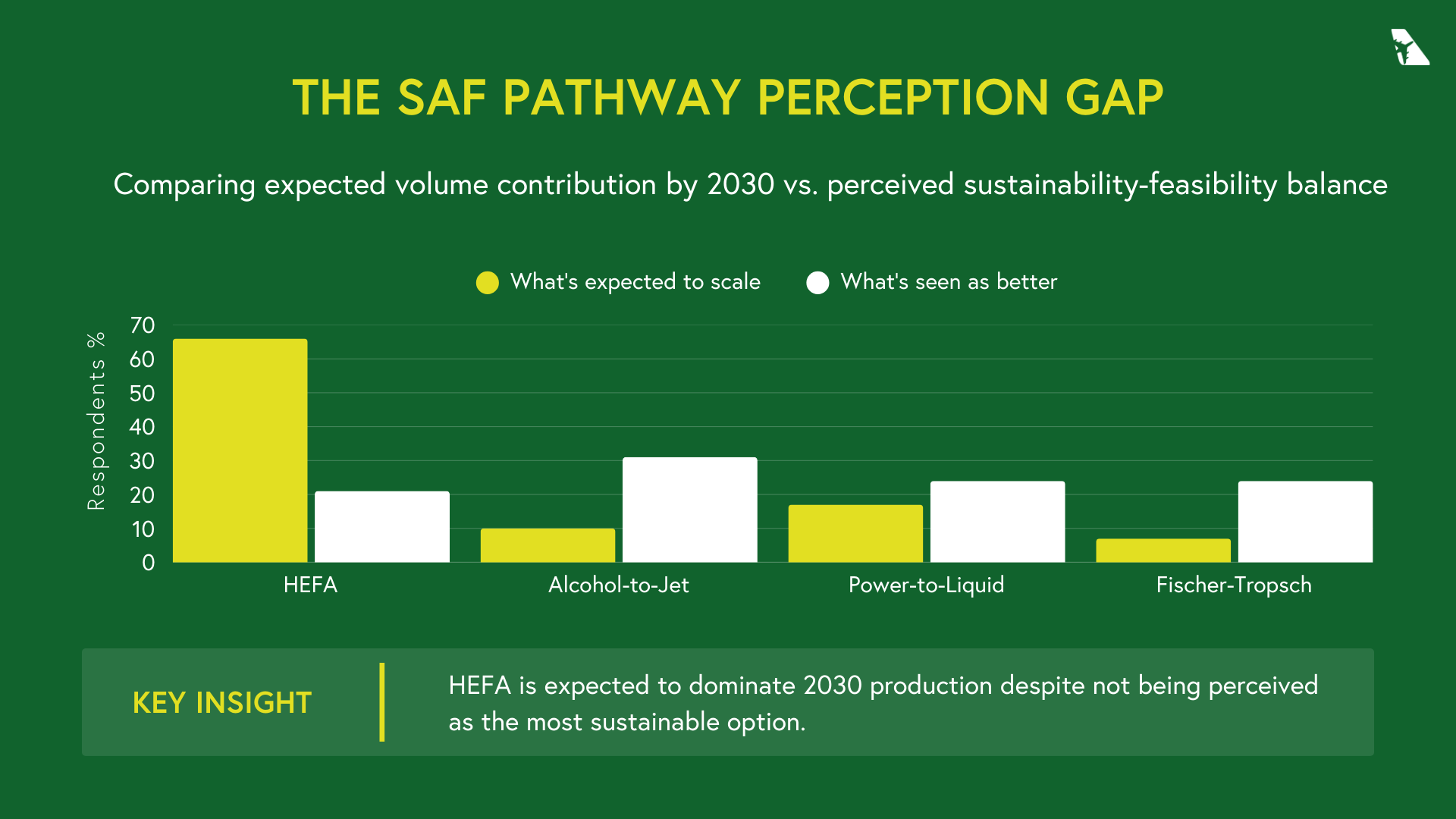

66% expect HEFA to dominate SAF production by 2030—but only 21% see it as the most sustainable option.

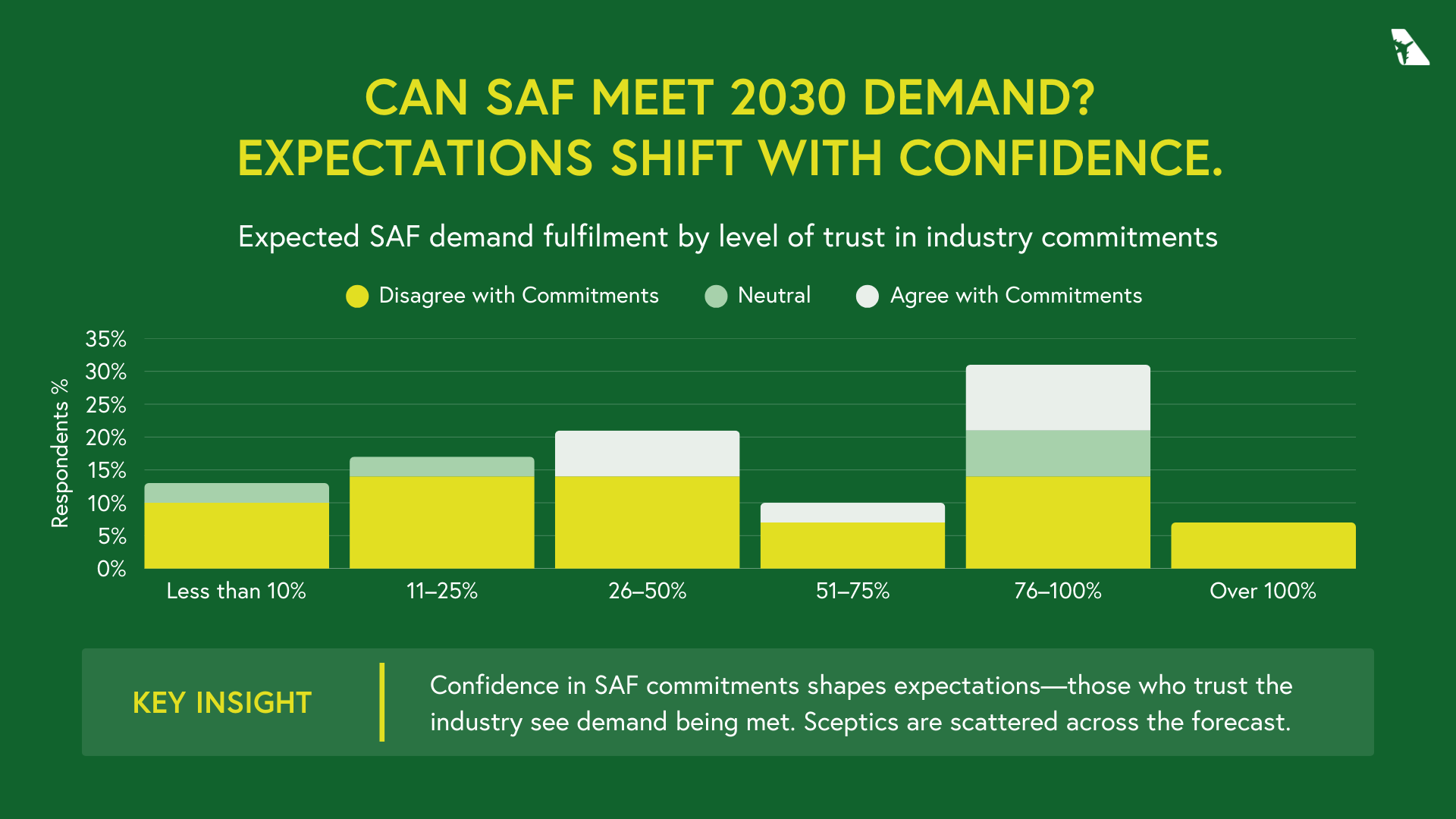

38% of respondents believe over 75% of SAF demand will be met by 2030—despite 66% doubting current industry commitments.

Transparency beats performance: clear carbon and feedstock tracking ranked as the top production priority.

Policy uncertainty is the top financing barrier—outweighing capital costs and fossil fuel competition.

Limited customer demand is the biggest non-cost hurdle to adoption.

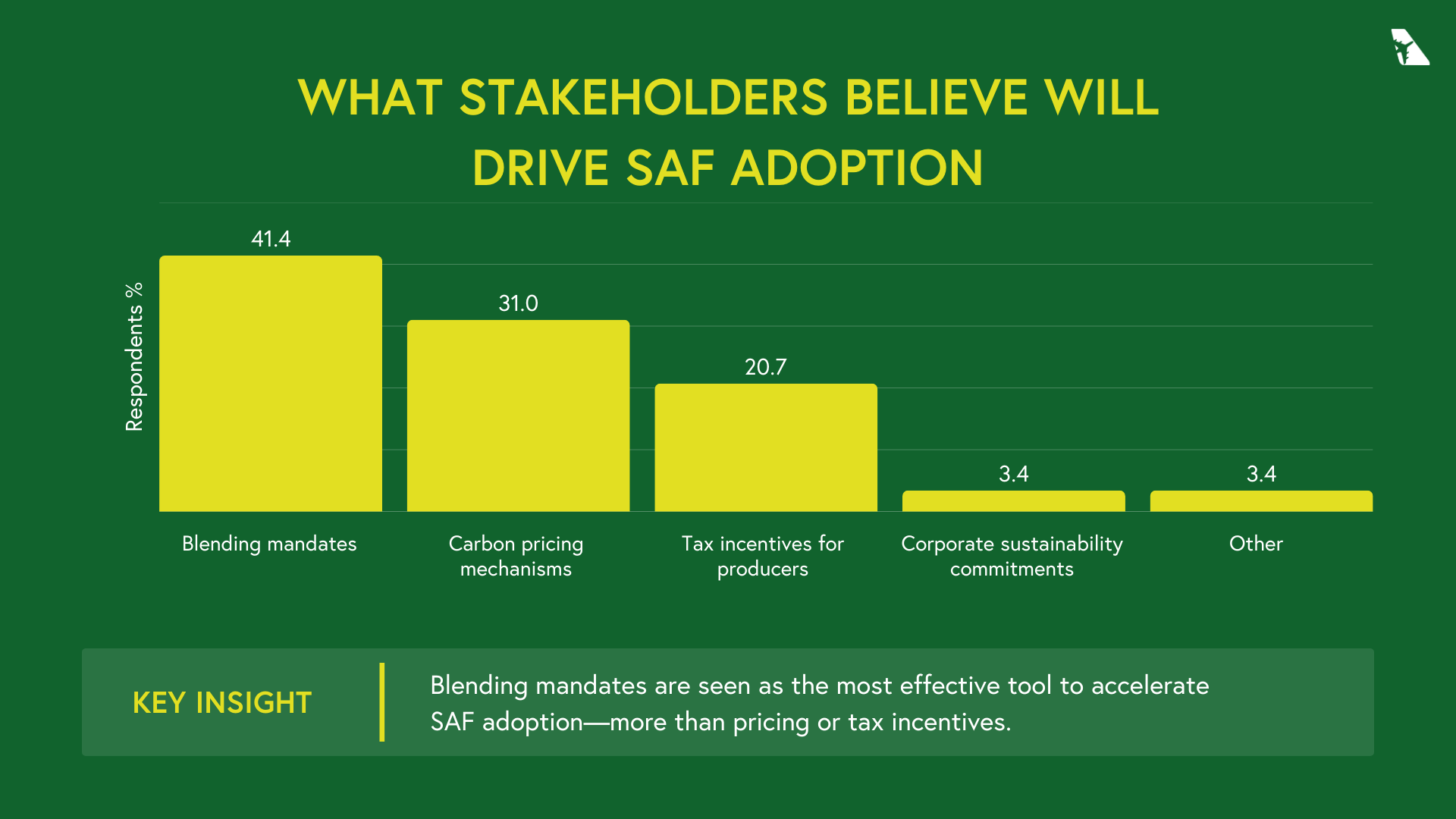

Mandates top the list of tools to accelerate SAF adoption—voluntary commitments rank last.

These responses sketch a picture of a sector in flux—one that recognises the urgency to scale SAF but is still grappling with uncertainty around technology choices, policy frameworks, and market demand.

Here’s a closer look at what these early signals might mean for the path ahead:

1. The production pathway paradox

SAF is expected to play a critical role in decarbonising aviation, but there’s a growing mismatch between what the industry is gearing up to produce, and what experts believe is actually sustainable and scalable in the long run.

The insight

Two-thirds (66%) of survey respondents expect HEFA to dominate SAF production by 2030. Yet only 21% believe it offers the best balance of sustainability and feasibility. Instead, respondents pointed to second-generation pathways like Alcohol-to-Jet (AtJ) and Power-to-Liquid (PtL) as more promising—but less likely to scale fast.

Dig deeper, and the divergence becomes more pronounced:

Producers were 2.5 times more likely than policy professionals to bet on HEFA, signalling a more cautious view on tech transition timelines from those building the infrastructure.

Meanwhile, those with the highest technical knowledge were far more likely to favour advanced pathways like AtJ—suggesting that deeper understanding correlates with stronger belief in next-gen solutions.

Together, this paints a picture of an industry at a crossroads: following the path of least resistance, while acknowledging it may not be the most future-proof.

The implication

The SAF market appears to be mirroring a classic innovation curve—early commercial winners (like HEFA) gain traction quickly, even as more sustainable alternatives struggle to move beyond pilot scale. But with increasing regulatory scrutiny, investor pressure, and feedstock limitations on the horizon, over-reliance on HEFA could lead to stranded assets or misaligned sustainability claims.

For producers, the challenge is technological. For policymakers, it’s strategic direction. And for investors, the question is whether the market is prepared to reward long-term alignment over short-term deliverability.

2. Big ambitions, shaky ground

Even as the industry debates how to scale SAF, another question looms: Will it scale at all—fast enough, and reliably enough?

Many stakeholders aren’t convinced. SAF production goals are ambitious, but there’s widespread doubt that current industry commitments are strong enough to support the level of investment required to meet them.

The insight

The majority of respondents (66%) expressed scepticism that today’s SAF commitments are sufficient to drive large-scale production investment. Yet, 38% still believe the industry will fulfil over 75% of the projected 2030 demand.

This gap reveals a kind of cognitive dissonance: the promises may lack credibility, but many still anticipate success—likely because they’re counting on external pressure, not internal resolve. Some of the strongest sceptics on commitment adequacy still expect high demand fulfilment, hinting at belief in looming regulatory enforcement rather than voluntary action.

The divide is also visible between stakeholder types:

Policy professionals were the most doubtful, with 7 out of 8 unconvinced by industry commitments.

Producers showed more mixed views, possibly balancing insider knowledge of investment timelines with optimism about demand signals.

Compounding this, views on the EU’s ReFuelEU Aviation Initiative suggest that most expect adoption to rise faster than production can keep up—highlighting a looming capacity crunch just as compliance pressure ramps up.

The implication

This split between belief and expectation creates uncertainty for investors and planners. If stakeholders assume regulation will “fix it,” but policies underdeliver or arrive late, the result could be severe supply bottlenecks or missed targets.

It also points to a bimodal investment climate, where some players plan cautiously based on current commitments, while others bet aggressively on fast policy-driven demand. Navigating that uncertainty—especially for SAF developers and financiers—will require clearer signals from both regulators and corporate buyers about long-term intent and enforcement.

3. Building confidence—from product to policy

Scaling SAF requires more than just facilities and feedstocks. The industry also needs trust—both in the sustainability of what’s being produced, and in the policy environment meant to support long-term investment. Right now, confidence in both areas is fragile.

The insight

When asked what matters most in SAF production—excluding cost and availability—respondents placed the highest priority on transparency. 38% pointed to clear tracking and verification of feedstocks and carbon emissions, ahead of carbon intensity, infrastructure compatibility, or energy efficiency. This indicates a shift toward proof-driven sustainability—where the ability to demonstrate claims is becoming just as important as the claims themselves.

This perspective was especially strong among airline procurement professionals and policymakers—those responsible for compliance, reporting, and public accountability. It also aligned closely with views on regulatory tools: respondents who prioritised transparency tended to support mechanisms like blending mandates, suggesting that credible verification and enforceable policy are seen as closely linked.

That theme carried over into financing concerns. When asked what’s holding back investment in new SAF capacity, 43% of respondents pointed to long-term policy uncertainty. Relatively fewer named capital costs (32%) or competition with conventional jet fuel (21%) as the primary barrier.

Producers were evenly split between cost and policy risk. But among policy professionals, there was near-unanimous concern: without stable regulation and clear timelines, even well-funded projects are difficult to justify. Many of these respondents also expressed doubt about the implementation of ReFuelEU—emphasising that how policy is delivered is as important as what it promises.

The implication

The SAF market is entering a phase where trust—in both product claims and policy frameworks—is central to progress. Verification mechanisms are moving from ‘nice-to-have’ to baseline expectation. Meanwhile, investors and producers are asking for clarity and consistency in the rules that govern long-term returns.

Without confidence in either domain, momentum stalls. For developers, this means integrating traceability and emissions data from the outset. For regulators, it means focusing not just on setting targets but on building the conditions for capital to follow.

4. Demand doubts and data gaps

Cost and supply have long dominated SAF conversations. But even if those barriers are addressed, deeper structural issues still threaten adoption—especially when it comes to customer behaviour and emissions tracking.

The insight

When asked about the biggest non-cost barriers to SAF uptake, 52% of respondents pointed to limited customer demand or pressure. Despite growing ESG rhetoric, many don’t see this translating into actual procurement behaviour. This disconnect casts doubt on the effectiveness of corporate climate commitments in moving the market.

Uncertainty around carbon accounting and emissions benefits (45%) emerged as another top barrier, suggesting technical concerns that cut across the value chain. Respondents cited challenges in tracking, verifying, and comparing lifecycle emissions across a growing number of feedstocks and technologies.

An equal share (45%) also pointed to a lack of clear mandates, reinforcing the view that policy clarity is still missing in key regions. Infrastructure limitations were highlighted by 31%—mostly by airline respondents—indicating practical constraints that may be underestimated upstream.

The implication

To truly scale SAF, the industry needs more than production and policy. It needs a demand signal backed by credible data and visible action. Standardising carbon accounting methodologies will be critical to reducing hesitation, especially among buyers. And turning ESG ambition into actual fuel contracts may require more direct engagement with corporate customers—paired with regulatory tools that leave less room for delay.

5. Mandates over market signals

So, what will it take to shift from hesitation to momentum? Everyone agrees SAF adoption needs to accelerate. But views differ on how to make that happen—and voluntary initiatives are rapidly losing credibility.

The insight

When asked which measures would be most effective for speeding up SAF uptake, 41% of respondents selected blending mandates, ahead of carbon pricing (31%) and tax incentives (21%). Producer organisations, often seen as opponents of rigid regulation, showed the strongest preference for mandates—challenging the notion that industry always favours flexibility.

Support for carbon pricing was more common among those who expressed confidence in industry commitments and demand fulfilment, suggesting a more optimistic view of market-driven mechanisms. Meanwhile, corporate sustainability pledges received almost no support as a meaningful acceleration tool—just one respondent selected it—revealing scepticism about the role of voluntary initiatives in driving real volume.

The implication

There’s a clear appetite for binding mechanisms that reduce uncertainty and guarantee demand. For regulators, this means mandates are no longer seen as a constraint, but a stabilising force—especially when combined with transparency requirements and credible enforcement. For market players still banking on soft commitments, the message is clear: policy-backed certainty is what will unlock real scale.

Our take

This survey offers an early look at where SAF conversations are headed and where action is still lagging. There’s broad agreement on the need to scale. But trust in current commitments, voluntary efforts, and policy execution remains low. Clearer signals are needed, and soon.

From production priorities to financing hurdles, the data points to a growing demand for proof: verifiable emissions data, stable policy frameworks, and credible buyer behaviour. Until those signals are stronger, the risk is that momentum will stall, despite all the ambition.

The path forward will require alignment—not just on targets, but on how the industry gets there. If these early signals are heeded, there’s still time to shift from hesitation to real progress.